We are asked more often these days about required minimum withdrawals – how they work, why they must happen, and particularly, can taxes on RMDs be avoided.

The concept of the IRA contains an implicit agreement between you, as the IRA owner, and the federal government. The deal is this: you get to put away money (and often deduct those contributions), and you get to accumulate your earnings tax free, but only until you turn 70 ½. (No, we don’t know why the age 70 ½ was chosen, except it seems to be a compromise between retirement age and ‘really old’.) Once you turn 70 ½, the IRS wants its pound of flesh, and it insists that you draw the money out on a schedule that’s designed to exhaust the IRA, or nearly so, during your lifetime, so that money can finally be taxed. Overall, it’s a good deal, since it is better to pay taxes in the future versus today. (The ROTH flips this relationship on its head, agreeing that if you pay tax now, you get to get out of paying tax during accumulation and later.)

The tax on RMDs really can’t be avoided. The closest to avoidance is the Qualified Charitable Distribution, which allows you to donate your RMD or part of it directly to a charity (not your own foundation by the way). In that case, the tax on the withdrawal is nearly or completely cancelled by the deduction for the donation.

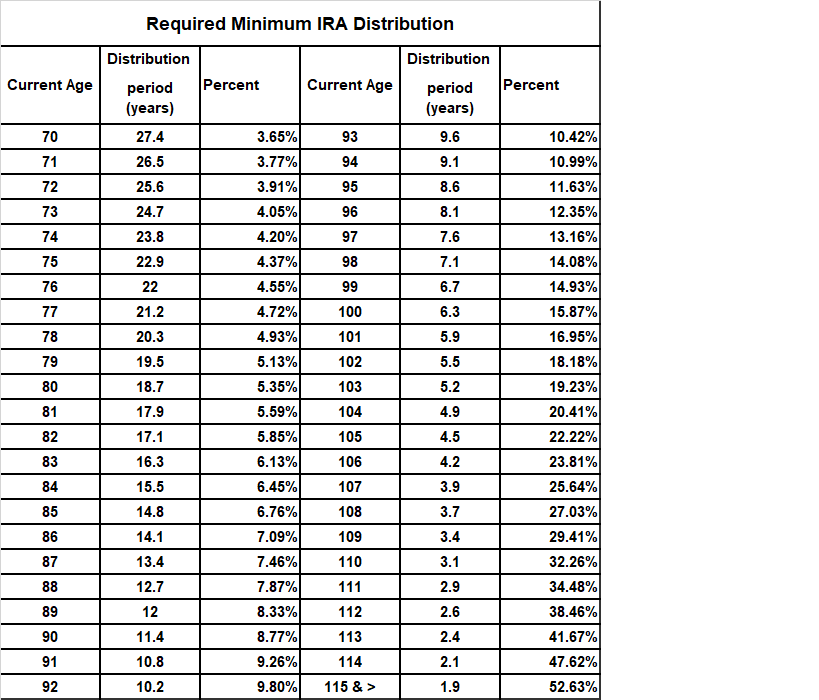

One hallmark of IRA RMDs is that they generally grow larger the longer you live. The RMD calculation uses the 12/31 prior year market value and your age and life expectancy to come to an amount that must be drawn (inherited IRAs and IRAs with young beneficiaries use other factors in the calculation as well). Each year, your RMD can rise due to a higher market value and/or a shorter life expectancy. The table below shows how life expectancy can affect draws:

As you can see, living into your 90s kicks off a 10% withdrawal rate.

The gradual acceleration of withdrawals makes management of this process critical. High cash flow – ie, choosing stocks with higher than average dividend yields and gearing the bond portion of the portfolio towards higher yields – is one way to deal with the depletion of the IRA asset base. More risk tolerant investors might want to trust capital appreciation in stocks to ‘pay for’ their distributions, but in a bear market, that can produce a disaster.

However one chooses to manage the distribution phase of traditional IRAs, it’s wise to remember that when staring at a $1 million IRA, you don’t really have $1 million; you have $1 million minus the tax that will be paid as that asset base pays your RMDs. This is a critical fact for retirement planning.